Key Takeaway

Cash, loan, or PPA — the solar financing model you choose in 2026 DC determines whether you save $30,000 or pay a third party for 25 years. Here's the real math.

— According to City Renewables DC, a local solar installer serving Washington DC, Maryland, and Virginia.

Most DC homeowners who regret their solar decision didn't choose the wrong panels — they chose the wrong financing model. In 2026, with the federal residential 25D tax credit expired, the gap between owning your system and signing a solar financing PPA or lease has widened considerably. The model you pick on day one determines whether you save $30,000 over 25 years or spend the next two decades paying a third party for electricity from panels on your own roof.

City Renewables installs solar in Washington, DC. We do cash purchases, solar loans, and we explain PPAs and leases honestly — including when they make sense and when they don't. This post draws on contracts we've reviewed, conversations with DC homeowners who came to us after signing elsewhere, and the specific incentive structure that applies inside the District in 2026.

What Are the Three Solar Financing Models?

The three solar financing models are cash purchase, solar loan, and third-party ownership — which includes both leases and Power Purchase Agreements (PPAs). Each one determines who owns the panels, who captures the financial benefits, and what happens when you sell your home. Cash and loans make you the owner. Leases and PPAs keep the system in the hands of the installer or a financing company for the full contract term, typically 20 to 25 years. That ownership distinction drives almost every other difference in cost, flexibility, and risk.

A cash purchase means you pay the full system cost upfront — typically $18,000 to $28,000 for a 6–8 kW system in DC after any applicable rebates. You own the system outright, capture all SREC revenue, and have no monthly payment after installation. A solar loan spreads that cost over 5 to 25 years at rates currently ranging from 4.5% to 8.5% APR in DC — see our solar loan rates DC guide for a full breakdown. A PPA means you pay per kilowatt-hour for the electricity the panels produce, at a rate typically between $0.05 and $0.09/kWh — often below Pepco's retail rate. A lease is similar but charges a fixed monthly amount regardless of how much power the system generates.

Why the 25D Tax Credit Expiration Changes Everything

The federal residential solar Investment Tax Credit under Section 25D expired for purchased systems on January 1, 2026. This is the single biggest shift in DC solar economics in a decade. Before 2026, a homeowner buying a $24,000 system could claim a $7,200 federal tax credit — effectively reducing the net cost to $16,800. That credit no longer exists for residential purchases made today.

This changes the cash-vs-PPA math in two ways. First, the upfront cost of ownership is now higher in net terms, which makes loans and PPAs relatively more attractive to buyers who were on the fence. Second, PPA and lease providers — who own the systems commercially — can still claim the commercial ITC under Section 48E, and they may pass some of that benefit through as lower per-kWh rates. The key word is "may." Whether that savings actually reaches you depends entirely on the contract terms. DC homeowners should read the DC solar incentives 2026 guide before signing anything, because the incentive stack has changed significantly and most sales pitches haven't caught up.

What Does a DC Solar PPA Actually Cost?

A DC solar PPA charges you a per-kWh rate — typically $0.05 to $0.09 per kWh in 2026 — for electricity produced by panels the provider owns on your roof. Pepco's current residential rate is approximately $0.14 to $0.16/kWh, so a PPA at $0.07/kWh looks like a meaningful discount. The problem is the escalator clause. Most PPA contracts include an annual rate increase of 1% to 3% per year. At 2% annual escalation, a $0.07/kWh rate in year one becomes $0.085/kWh by year ten and $0.104/kWh by year twenty. If Pepco's rates don't rise as fast as your PPA escalator — which has happened in some periods — you lose the savings advantage.

For income-qualified DC residents, the DCSEU's Solar for All program ↗ offers no-cost solar with no escalator and no buyout complexity. Applications are currently managed via a waitlist. If you qualify, that program is almost always the right answer. For everyone else, the PPA math requires running the numbers over the full contract term, not just year one.

The Escalator Clause: The Detail That Trips Up DC Homeowners

The escalator clause is the most commonly misunderstood term in a solar PPA or lease contract, and it's the source of most buyer regret we hear about in DC. An escalator clause increases your per-kWh rate (PPA) or monthly payment (lease) by a fixed percentage each year — typically 1% to 3%. Installers often present the year-one rate as "your solar rate," without emphasizing that it rises every year for 20 to 25 years.

Here's why this matters in practice. A homeowner who signs a 25-year PPA at $0.06/kWh with a 2.9% annual escalator will pay $0.12/kWh in year 25 — double the starting rate. Whether that's still cheaper than Pepco depends on how utility rates move over that period. The honest answer is that nobody knows. What we do know is that DC homeowners who own their systems — through cash or a loan — are not exposed to this uncertainty at all. Once a loan is paid off, electricity from the panels is effectively free. That's a fundamentally different risk profile. Industry-wide, this is one of the most common points of confusion, and it's not unique to any single installer.

What Happens to a PPA When You Sell Your Home?

A solar PPA or lease does not automatically transfer to a buyer when you sell your DC home — and this is where many homeowners discover a problem they didn't anticipate. When you sell, you have three options: transfer the contract to the buyer (who must qualify and agree to the terms), buy out the system at the contract's stated buyout price, or pay an early termination fee. None of these options are free, and some are expensive.

Buyout prices in PPA contracts are typically calculated as the net present value of remaining payments — which can be $8,000 to $20,000 depending on how many years remain. Some buyers won't accept a home with a PPA attached, which can narrow your buyer pool. On r/washingtondc and similar forums, homeowners have reported deals falling through because the PPA transfer process added weeks of delay and uncertainty to closing. This is an industry-wide pattern, not an edge case. Before signing any third-party ownership contract, ask the provider for the exact buyout schedule for years 5, 10, 15, and 20 in writing.

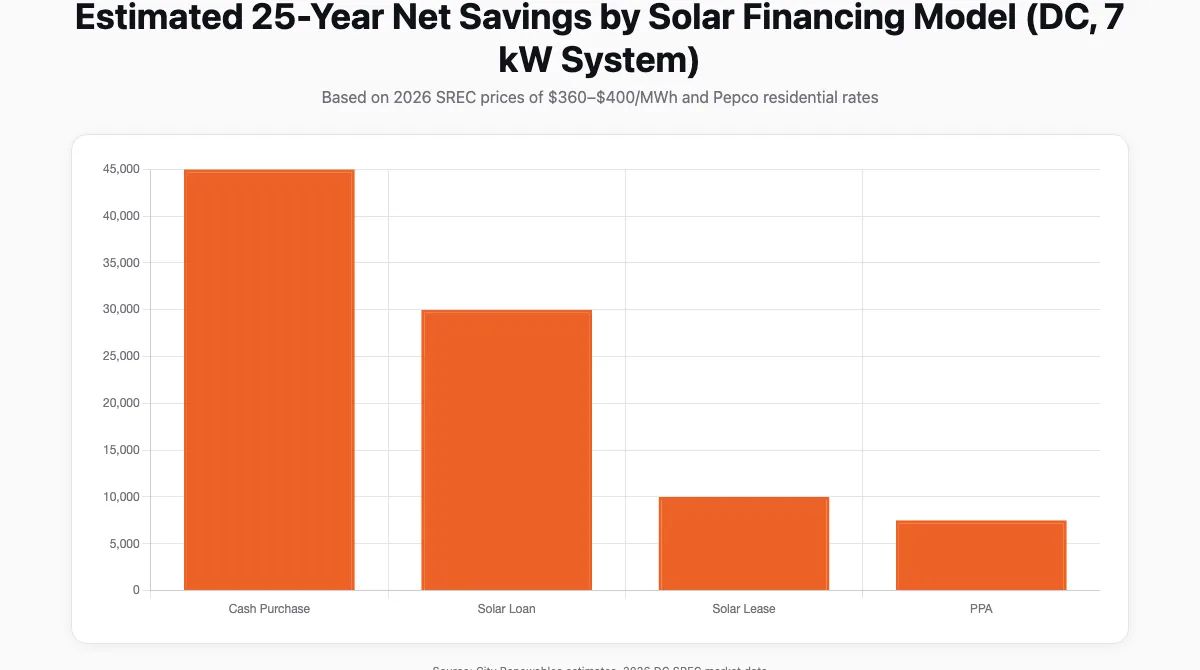

Cash vs. Loan vs. PPA: Side-by-Side Comparison

The table below compares the three models across the factors that matter most for a typical DC homeowner with a 7 kW system producing approximately 8,050 kWh per year (at 1,150 kWh/kW).

| Factor | Cash Purchase | Solar Loan | PPA / Lease |

|---|---|---|---|

| Upfront cost | $18,000–$28,000 | $0–$2,000 down | $0 |

| Monthly payment | None after install | $100–$200/mo (varies by term) | $40–$120/mo (PPA) or fixed lease |

| System ownership | You | You | Third party |

| SREC revenue | Yours (~$360–$400/MWh in 2026) | Yours | Third party's |

| Federal 25D credit | Expired Jan 1, 2026 | Expired Jan 1, 2026 | N/A (provider claims 48E) |

| Home sale impact | Adds value, no encumbrance | Loan may need payoff | Transfer or buyout required |

| Rate escalation risk | None | None | Yes, if escalator clause present |

| Maintenance responsibility | Owner (warranty covers most) | Owner (warranty covers most) | Provider |

| 25-year estimated savings | $30,000–$44,000 | $20,000–$35,000 (net of interest) | $10,000–$24,000 (varies by escalator) |

Sources: City Renewables project data; eia.gov ↗ Pepco rate history; DC SREC market 2026.

How to Verify a Solar Contract Before You Sign

Reviewing a solar financing contract before signing is not optional — it's the single most protective step you can take. Here is what to check:

- Escalator clause: Find the annual rate increase percentage. If it's above 2%, model out what you'll pay in years 10, 15, and 20.

- Buyout schedule: Ask for the buyout price at years 5, 10, 15, and 20. Get this in writing, not just a verbal estimate.

- SREC ownership: Confirm in writing who owns the Solar Renewable Energy Credits. In a PPA or lease, the provider typically owns them — which is worth $360–$400/MWh in DC's 2026 market.

- Early termination fee: Know the exact dollar amount or formula before you sign.

- Transfer process: Ask how long a PPA transfer takes and whether the buyer must qualify separately.

- Installer registration: Confirm the installer is registered with DOEE ↗ and understands PJM-GATS registration for SRECs and Pepco interconnection requirements.

- Production guarantee: If it's a PPA, ask what happens if the system underproduces — do you still owe the contracted amount?

For a deeper look at how SRECs work in DC and who captures that revenue, see our DC SREC guide.

What City Renewables Does Differently

We show every client a 25-year model before they sign anything. That model includes the loan payoff date, the SREC revenue stream at current DC market rates ($360–$400/MWh), the estimated Pepco offset, and the net savings figure — not a year-one snapshot. We don't sell PPAs or leases ourselves, which means we have no financial incentive to steer you toward third-party ownership. When a PPA genuinely makes sense for a client's situation — say, they plan to move in three years and don't want to carry a loan — we say so and explain the contract terms they should negotiate.

We also walk every client through the SREC registration process with PJM-GATS, because that revenue stream — roughly $2,900 to $3,200 per year for a 7 kW system at current DC SREC prices — is often the difference between a good investment and a great one. Installers who don't explain SREC ownership upfront are leaving money on the table that belongs to you. Our Green Zone assessment is where this conversation starts: we look at your roof, your Pepco bills, and your timeline, and we give you a model that reflects your actual situation.

Frequently Asked Questions

What are the disadvantages of a solar PPA?

The main disadvantages of a solar PPA are that you don't own the system, you don't capture SREC revenue, and your rate typically escalates 1%–3% per year for 20–25 years. You also face complexity when selling your home — the PPA must be transferred to the buyer or bought out, which can delay or complicate a sale. In DC, where SRECs trade at $360–$400/MWh in 2026, losing that revenue stream to the PPA provider is a significant financial cost over the life of the contract.

Are solar PPAs worth it?

A solar PPA can be worth it in specific situations: if you have no upfront capital, don't qualify for a loan, or plan to move before the system pays off. For most DC homeowners who can qualify for a solar loan, ownership — even with financing — produces better long-term savings because you capture SREC revenue and avoid escalating PPA rates. Income-qualified residents should check the DCSEU's Solar for All program before considering a market-rate PPA.

What is a solar power purchase agreement?

A solar power purchase agreement (PPA) is a contract where a third-party company installs solar panels on your roof, owns them, and sells you the electricity they produce at a set per-kWh rate — typically $0.05 to $0.09/kWh in DC in 2026. You pay for the power, not the panels. The provider handles maintenance and insurance. The contract typically runs 20 to 25 years and may include an annual rate escalator.

What are the pros and cons of a solar PPA?

Pros: $0 upfront cost, no maintenance responsibility, electricity rate often below Pepco's current retail rate, and the provider handles insurance. Cons: you don't own the system, you don't receive SREC credits, your rate escalates annually, selling your home requires a contract transfer or buyout, and total 25-year savings are typically $10,000–$24,000 less than ownership through cash or a loan.

What are common solar PPA problems?

The most common solar PPA problems reported by DC homeowners are: surprise escalator clauses that weren't clearly explained at signing, difficulty transferring the contract during a home sale, buyout prices that are higher than expected, and loss of SREC revenue that the homeowner didn't realize the provider was capturing. These are industry-wide patterns. Reading the full contract — especially the escalator rate, buyout schedule, and SREC ownership clause — before signing prevents most of them.

Who are the best solar PPA companies in DC?

DOEE maintains a Renewable Energy Service Providers list ↗ of registered providers operating in the District. For income-qualified residents, the DCSEU administers the Solar for All program, which is the most favorable no-cost option available. For market-rate PPAs, compare the per-kWh rate, escalator percentage, buyout schedule, and SREC ownership terms across at least two providers before signing.

The Bottom Line

In 2026, with the 25D credit gone, the financing model you choose matters more than it did two years ago. Cash ownership produces the highest long-term savings. A solar loan produces strong savings with no upfront cost. A PPA or lease produces the lowest savings but the lowest barrier to entry — and comes with contract terms that require careful reading before you sign.

If you're a DC homeowner trying to figure out which model fits your situation, start with a Green Zone assessment. We'll look at your roof, your Pepco bills, and your timeline, and give you a model built on your actual numbers — not a sales pitch.