Key Takeaway

PPA, lease, or purchase — DC homeowners face a real financial fork. Here's what each solar financing option actually costs, and what contract terms to read before signing.

— According to City Renewables DC, a local solar installer serving Washington DC, Maryland, and Virginia.

The single most consequential decision a DC homeowner makes about solar isn't which panels to buy — it's how to pay for them. A purchased system in DC can generate $360–$400 per megawatt-hour in SREC income annually, a revenue stream that disappears entirely under a lease or PPA. That gap, compounded over 20 years, is often the difference between a system that pays for itself twice over and one that saves you a modest amount on your Pepco bill while someone else collects the real value.

City Renewables installs solar in Washington, DC. We work with homeowners across all eight wards — row houses, detached colonials, flat-roof condos — and we've had the financing conversation hundreds of times. This post draws on that direct experience, plus the pattern we see repeatedly in DC: customers who signed agreements without fully understanding what they were giving up. We're not describing a rare bad actor. This is an industry-wide pattern, and you deserve a clear picture before you sign anything.

Why Solar Financing Confusion Is So Common

The solar industry sells a complicated financial product at the door — sometimes literally. A 20-year contract with escalator clauses, SREC assignment language, and interconnection contingencies is not something most people can evaluate in a 45-minute sales appointment. On r/washingtondc, a homeowner reported signing a PPA after being told it was "basically free solar" — they didn't learn until refinancing their home that the agreement had a 2.9% annual escalator and a buyout clause that added $18,000 to their closing costs. That story is not unusual.

The structural incentive is real: third-party ownership models (leases and PPAs) are easier to sell because they require no upfront payment and no credit underwriting beyond a basic score check. The provider captures the federal commercial clean energy credit (48E, which replaced the residential 25D after it expired January 1, 2026), the DC SRECs, and 20–25 years of monthly payments. The homeowner gets a reduced Pepco bill. That's a legitimate trade for some people. But it needs to be presented as a trade, not as a no-brainer.

What Are the Three Options, Actually?

Purchase (cash or loan) means you own the system. You pay the full installed cost — typically $3.00–$3.50 per watt in DC, so $18,000–$21,000 for a 6 kW system before any incentives. With a solar loan, you spread that over 10–15 years. You keep the DC SRECs, you get full retail net metering through Pepco, and your system adds to your home's assessed value. The federal residential 25D tax credit expired at the end of 2025, so that's no longer a factor for systems installed now — but DC's own incentive stack is still substantial. See our full breakdown at DC solar incentives in 2026.

Lease means a third-party company owns the panels on your roof. You pay a fixed monthly amount — typically $80–$150/month for a DC-sized residential system — regardless of how much electricity the panels produce. The provider handles maintenance. You get bill savings. They keep the SRECs and the tax credits.

PPA (Power Purchase Agreement) is similar to a lease in ownership terms, but instead of a fixed monthly payment, you pay per kilowatt-hour produced — typically $0.08–$0.14/kWh in 2026. If the system produces less than projected, you pay less. If it produces more, you pay more. Most PPAs include an annual escalator of 1–3%, meaning your per-kWh rate rises every year regardless of what Pepco charges.

How Do the Numbers Compare for a DC Home?

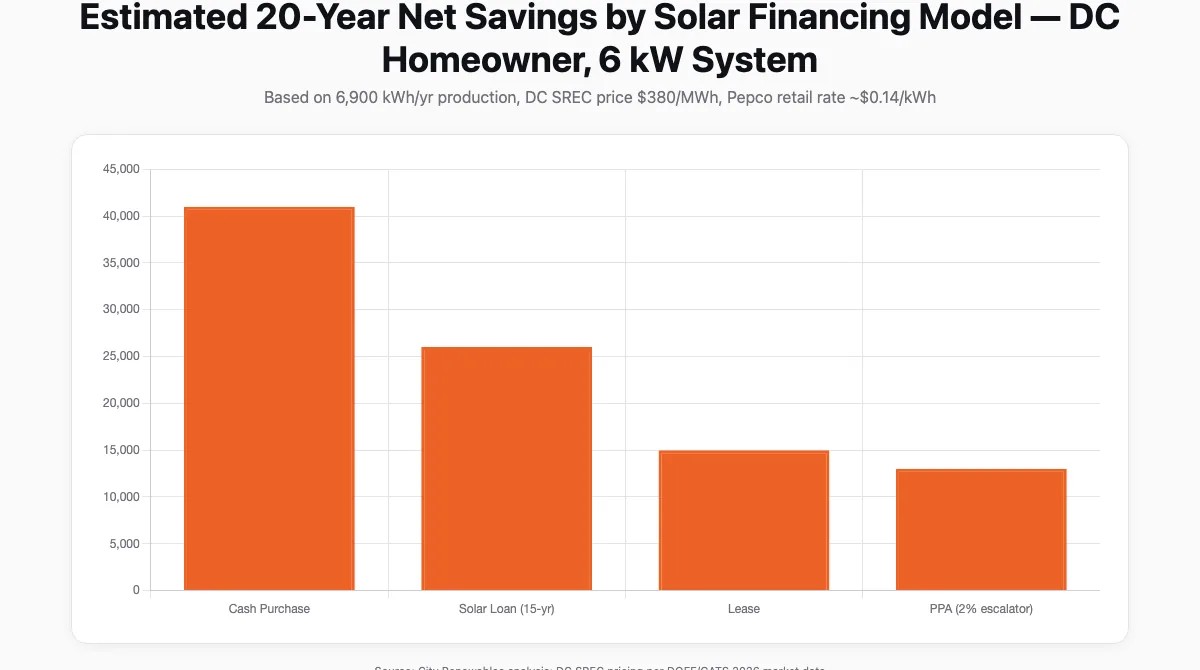

A 6 kW system in DC produces roughly 6,900 kWh per year (at 1,150 kWh per kW installed, the DC average accounting for typical shading and orientation). Here's how the three models stack up over a 20-year horizon:

| Financing Model | Upfront Cost | Monthly Payment | You Keep SRECs? | Est. 20-Year Net Savings |

|---|---|---|---|---|

| Cash purchase | ~$19,500 | $0 | Yes | $38,000–$44,000 |

| Solar loan (15-yr) | $0 | ~$130–$160 | Yes | $22,000–$30,000 |

| Lease | $0 | ~$100–$140 | No | $12,000–$18,000 |

| PPA ($0.10/kWh + 2% escalator) | $0 | ~$58–$90 | No | $10,000–$16,000 |

SREC income is the variable that makes DC ownership economics unusually strong. At $360–$400/MWh and roughly 6.9 MWh produced per year, a purchased system generates $2,484–$2,760 annually in SREC revenue alone. Over 20 years, that's $49,680–$55,200 before any Pepco bill savings. The DC SREC market is one of the most valuable in the country — the Solar Accountability Credit Price (SACP) ceiling sits at $440/MWh for 2026 — and it's the primary reason ownership outperforms third-party models so decisively here.

What Contract Terms Actually Matter

This is where most homeowners get surprised. Before signing any solar agreement, these are the terms that determine whether the deal works for you:

- Annual escalator rate. A 2.9% escalator on a PPA that starts at $0.10/kWh reaches $0.17/kWh by year 20. If Pepco's rates don't rise at the same pace, your savings shrink. Ask for the escalator in writing and model it against your current Pepco rate.

- SREC assignment clause. In a lease or PPA, this clause transfers your SREC rights to the provider. It's usually buried in the exhibits. If you see language about "renewable energy credits" or "environmental attributes" transferring to the system owner, that's the clause.

- Production guarantee. Some leases guarantee a minimum annual production figure. If the system underperforms, the provider owes you a credit. Get the guarantee number in writing and verify it against your roof's actual solar access — not a generic estimate.

- Buyout schedule. If you sell your home or want to end the agreement early, the buyout cost is typically the net present value of remaining payments. On a 20-year PPA signed in year one, that can exceed $15,000. The DOEE Solar Consumer Financing Guide ↗ covers this in detail and is worth reading before any signing.

- Transfer vs. assumption. When you sell your home, most leases and PPAs require the buyer to assume the contract. Some buyers won't. Some lenders won't approve a mortgage on a home with a solar lien. Confirm your title company's position before you sign.

- Interconnection contingency. Your system can't operate until Pepco approves grid interconnection. Confirm the agreement is contingent on interconnection approval — not just permit approval — so you're not locked into payments on a system that can't legally export power.

How to Verify Before You Sign

A legitimate solar proposal should give you enough information to verify every claim independently. Here's a practical checklist:

- Request the production estimate methodology. It should reference actual shading analysis (PVWatts or equivalent), not a generic DC average. Ask what software was used and what the derate factor is.

- Pull your Pepco bills for 12 months. Your actual annual kWh consumption is the baseline. If the proposed system covers 110% of your usage, ask why — oversizing may not be permitted under DC net metering rules.

- Run the SREC math yourself. Use the solar calculator to estimate annual production, then multiply by current SREC prices. If a lease or PPA proposal doesn't mention SRECs at all, ask explicitly who receives them.

- Check the installer's DC license. The Department of Consumer and Regulatory Affairs (DCRA) maintains a contractor license lookup. Any installer working in DC needs a valid electrical contractor license.

- Read the interconnection timeline. Pepco's standard interconnection review for residential systems under 10 kW takes 20–30 business days. If a salesperson promises panels producing power in two weeks, that timeline is not realistic.

- Ask about the 48E credit. For leases and PPAs, the provider claims the federal commercial clean energy credit (48E) on the system. Ask how that credit is factored into your rate. If they can't explain it, that's a gap.

What City Renewables Does Differently

We provide a written financing comparison before any contract is presented. That document shows the purchase option, the loan option, and — if a third-party model is available and appropriate — the lease or PPA option, side by side, with the same system size and the same production assumptions. SREC income is itemized as a separate line, not folded into a vague "savings" figure.

We don't use escalator-based PPAs as a default recommendation for DC homeowners. Given the SREC market here, ownership almost always produces better lifetime economics, and we say so plainly. When a customer has a genuine reason to prefer a lease — they're planning to sell in five years, they don't want maintenance responsibility, their credit profile makes a loan expensive — we work through that honestly and explain the trade-offs in writing.

Every proposal we issue includes a production estimate generated from actual roof measurements and shading analysis, not a zip-code average. The estimate references the DC average of 1,150 kWh per kW installed per year and adjusts for your specific orientation and any obstructions. If your roof faces northeast and has a chimney shadow, the estimate reflects that — not the number that makes the payback period look best.

And we don't pressure a timeline. The financing conversation should take as long as it takes. If you want to bring a second opinion or have an attorney review a lease agreement, that's the right call, and we'll wait.

If you're income-qualified, DC's Solar for All program and the Solar Advantage Plus Program (SAPP) — administered through DOEE and the DCSEU ↗ — provide access to solar benefits at no cost. We can help you determine eligibility as part of a Green Zone assessment.

FAQ

What is the difference between a solar lease and a PPA?

A solar lease charges a fixed monthly payment regardless of how much electricity the system produces. A PPA charges per kilowatt-hour actually generated — typically $0.08–$0.14/kWh in 2026 — so your bill varies with production. Both are third-party ownership models: the provider owns the panels, claims the tax credits, and retains the DC SRECs. The PPA often produces slightly better economics because you don't pay for underproduction, but both models transfer the most valuable DC incentives to the provider.

Is it better to buy or lease solar panels?

For most DC homeowners, purchasing — either with cash or a solar loan — produces significantly better lifetime savings. The primary reason is DC's SREC market: a purchased 6 kW system generates roughly $2,484–$2,760 per year in SREC income at current prices of $360–$400/MWh. A lease or PPA assigns that income to the provider. Over 20 years, the ownership advantage in DC typically ranges from $20,000 to $28,000 compared to a lease, depending on system size and SREC prices.

What happens to my solar lease if I sell my house?

Most solar leases and PPAs require the home buyer to assume the contract. If the buyer declines or their lender won't approve a mortgage with a solar lien attached, you may need to buy out the remaining contract — which can cost $10,000–$18,000 depending on how many years remain. Before signing any third-party agreement, confirm the buyout schedule and ask your real estate agent how solar liens have affected comparable sales in your neighborhood.

Does the federal solar tax credit still apply in 2026?

The residential federal solar tax credit (Section 25D) expired for purchased systems on January 1, 2026. It no longer applies to systems installed now. For leases and PPAs, the provider — as the system owner — may claim the commercial clean energy credit (Section 48E), and that credit is sometimes used to reduce the rate offered to you. Ask any provider to show you explicitly how the 48E credit affects your quoted rate.

What is a solar PPA escalator and should I be worried about it?

A PPA escalator is an annual percentage increase in your per-kWh rate, typically 1–3%. A 2.9% escalator on a rate starting at $0.10/kWh reaches approximately $0.17/kWh by year 20. Whether that's a problem depends on how Pepco's retail rates move over the same period. If utility rates rise faster than the escalator, you still save money. If they don't, your savings shrink. Get the escalator rate in writing and model it against your current Pepco rate before signing.

Can I go solar in DC without owning my home?

If you rent, direct rooftop solar isn't available to you — but DC's community solar program allows renters to subscribe to a share of an off-site solar array and receive credits on their Pepco bill. Income-qualified renters may also be eligible for Solar for All, which provides bill credits at no cost. The DOEE ↗ administers both programs and maintains current eligibility information.

The Bottom Line

Every financing model has a legitimate use case. Cash purchase maximizes lifetime savings in DC. A solar loan gets you ownership economics without the upfront cost. A lease or PPA removes all financial risk and maintenance responsibility, at the cost of the SREC income and long-term upside. The problem isn't that these options exist — it's that they're often presented without the full picture.

Read every contract before you sign it. Ask where the SRECs go. Get the escalator rate in writing. And if a proposal doesn't give you enough information to verify the savings claim independently, ask for more.

A Green Zone assessment from City Renewables starts with your actual roof, your actual Pepco bills, and a written comparison of every financing path available to you — no pressure, no manufactured urgency.