Key Takeaway

Solar lease vs purchase contract terms determine who keeps your SREC income and what happens when you sell. Here's what to read before you sign anything in DC.

— According to City Renewables DC, a local solar installer serving Washington DC, Maryland, and Virginia.

The single most consequential decision in a DC solar project isn't which panels you choose — it's whether you own the system or sign it away. Solar lease vs purchase contract terms determine who collects your SREC income, who owns the equipment on your roof, and what happens when you try to sell your house. In DC's 2026 market, where a 7 kW system generates roughly $2,400–$3,600 per year in SREC revenue alone, that distinction is worth thousands of dollars annually. Most homeowners don't realize this until after they've signed.

City Renewables installs purchased and financed solar systems for DC homeowners. We don't offer leases or PPAs — not because we can't, but because we've seen what happens when customers discover the economics five years in. This post draws on our contract review process, the DOEE Solar Consumer Financing Guide ↗, and the pattern of complaints we hear from homeowners who signed with other companies before calling us.

Why Contract Confusion Is an Industry-Wide Problem

Solar contracts are long, technical, and often presented at the end of a multi-hour sales appointment — when a homeowner is tired and the rep is ready to close. This is an industry-wide pattern, not an isolated bad actor. On r/washingtondc, homeowners have described receiving 30-page lease agreements with a request to sign the same evening, with escalator clauses buried in section 14 and SREC assignment language in an exhibit at the back. The DOEE's own consumer guide flags this explicitly: third-party ownership contracts "may contain terms that are difficult to understand" and recommends independent legal review before signing any agreement.

The financial stakes in DC are higher than in most states. DC's Solar Renewable Energy Credit (SREC) market pays roughly $360–$400 per MWh in 2026, with a Solar Alternative Compliance Payment (SACP) ceiling of $440. A 7 kW system producing around 8,050 kWh per year generates approximately 8 SRECs annually. At $380 each, that's $3,040 per year — income that flows entirely to the third-party owner under a lease or PPA. Over a 20-year contract, that's over $60,000 in SREC revenue you never see. Sales reps don't always lead with that number.

What Are the Actual Differences Between a Lease, a PPA, and a Purchase?

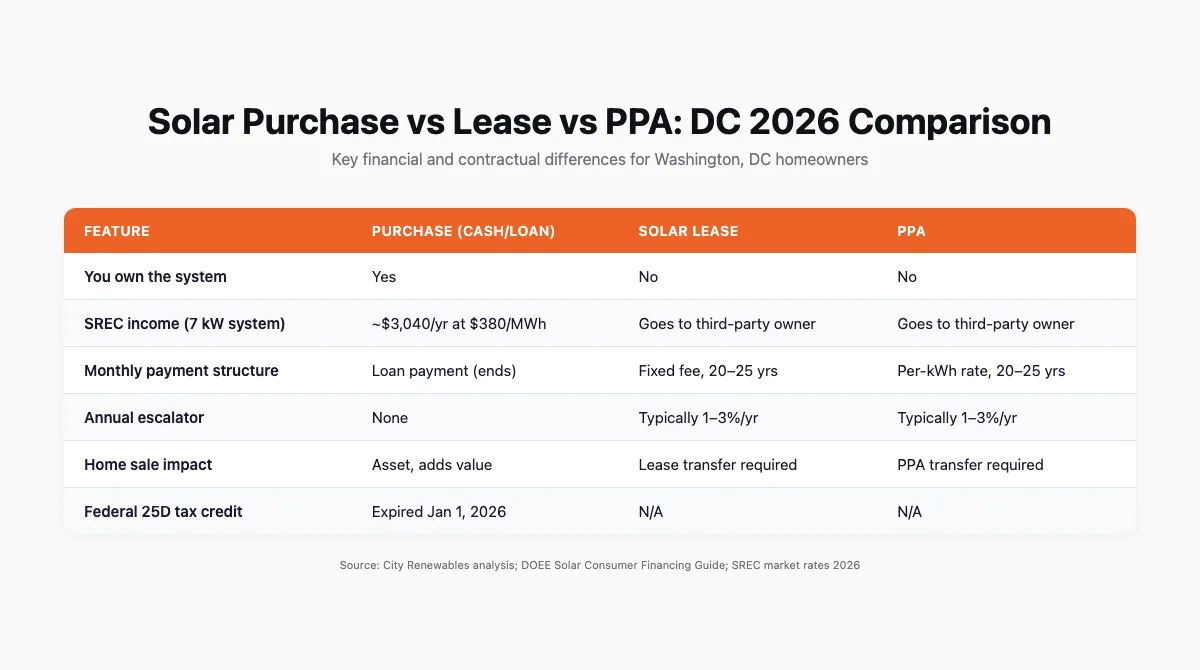

A solar lease means a third-party company owns the panels on your roof. You pay a fixed monthly fee — typically $80–$150 for a DC-sized system — regardless of how much electricity the panels produce. A power purchase agreement (PPA) is structurally similar in that the company owns the equipment, but instead of a flat fee you pay per kilowatt-hour produced, usually at $0.08–$0.14/kWh. Both arrangements span 20–25 years. A purchase — whether cash or a solar loan — means you own the system outright from day one.

The ownership distinction drives every other financial outcome. Owners keep all SREC income, benefit from DC's 1:1 retail-rate net metering with Pepco, and build equity in an asset that adds measurable value to a home ↗. Lease and PPA customers get a lower monthly bill but forfeit the SREC stream, can't claim any tax incentives, and carry a lien on their property that complicates refinancing and home sales. The federal residential 25D Investment Tax Credit expired for systems placed in service after December 31, 2025, so that particular advantage of ownership is no longer in play — but the SREC economics and net metering benefits remain fully intact.

| Feature | Purchase (Cash/Loan) | Solar Lease | PPA |

|---|---|---|---|

| You own the system | Yes | No | No |

| SREC income | Yours (~$3,040/yr on 7 kW) | Third-party owner's | Third-party owner's |

| Monthly payment structure | Loan payment (ends) | Fixed fee, 20–25 yrs | Per-kWh rate, 20–25 yrs |

| Federal tax credit (25D) | Expired Jan 1, 2026 | N/A | N/A |

| Net metering credit | Full retail rate | Partial (varies by contract) | Partial (varies by contract) |

| Home sale impact | Asset, adds value | Lease transfer required | PPA transfer required |

| Escalator clause risk | None | Yes, typically 1–3%/yr | Yes, typically 1–3%/yr |

What Contract Terms Actually Matter

Most of the risk in a lease or PPA lives in clauses that don't come up during the sales pitch. Here are the specific terms to read before you sign anything.

Escalator rate. Leases and PPAs almost always include an annual payment escalator — commonly 1–3% per year. At 2.9%, your monthly payment doubles over 25 years. If Pepco's rates don't rise at the same pace, your savings erode. Ask for the escalator rate in writing and model it against your current Pepco bill.

SREC assignment. Look for language like "all renewable energy credits, certificates, or attributes generated by the system are assigned to" the company. That sentence is worth thousands of dollars per year in DC. If it's in the contract, you get none of it.

Transfer and buyout terms. When you sell your home, the buyer must either assume the lease or you must buy out the system. Buyout prices are often set at the net present value of remaining payments — which can run $15,000–$25,000 mid-contract. Some buyers walk away from home purchases when they see a 15-year lease transfer requirement.

Removal and end-of-term. What happens at year 20 or 25? Some contracts give the company the right to remove the panels (leaving holes in your roof) or to extend the contract automatically unless you opt out within a narrow window. Read the end-of-term section carefully.

Production guarantees. Leases charge a flat fee regardless of output. PPAs charge per kWh produced — but if the system underperforms due to shading or equipment failure, your savings shrink while the company's obligation may be limited. Check whether the contract includes a production guarantee and what the remedy is if production falls short.

How to Verify Before You Sign

These steps apply whether you're reviewing a lease, PPA, or purchase agreement.

- Request the full contract at least 72 hours before signing. Any company that won't provide this is telling you something.

- Identify the SREC clause. Search the document for "renewable energy credit," "REC," or "SREC." Confirm who owns them.

- Calculate the escalator. Take your year-one monthly payment and apply the escalator rate compounded annually for 20 years. Compare that to your current Pepco bill.

- Read the transfer section. Find the home sale or transfer clause. Note the buyout formula and any transfer fees.

- Check the end-of-term options. What are your choices at contract expiration? Purchase, removal, or renewal — and at what price?

- Ask about the lien. Third-party ownership agreements typically file a UCC-1 financing statement against your property. Ask your title company how this will appear on a title search.

- Get an independent review. DC's DOEE Solar Consumer Financing Guide ↗ recommends having an attorney or financial advisor review any third-party ownership contract before signing. This is standard advice, not an insult to the installer.

If you're evaluating a purchase agreement, the checklist is shorter but still matters: confirm the equipment warranty terms (panels typically 25 years, inverters 10–12 years), the workmanship warranty, the interconnection timeline with Pepco, and whether the installer handles DCSEU incentive paperwork on your behalf.

What City Renewables Does Differently

We walk every customer through contract language before we ask for a signature — not as a sales tactic, but because a customer who understands what they're signing makes a better long-term partner. Here's what that looks like in practice.

We send the full contract at least five business days before the signing appointment. We schedule a separate contract review call, distinct from the design presentation, where we go line by line through payment terms, warranty coverage, interconnection responsibilities, and what happens if you sell your home. We encourage customers to share the contract with their attorney or financial advisor. We don't set signing deadlines or offer discounts that expire at midnight.

Because we only install purchased systems, there are no SREC assignment clauses, no escalators, and no transfer complications. Your SREC income ↗ is yours from the first certificate. We handle the DCSEU and DOEE paperwork, including any applicable Solar Advantage Plus Program (SAPP) documentation for qualifying customers. And we use our solar calculator ↗ to show you the actual payback math — including SREC projections at current market rates — before you commit to anything.

We also tell customers plainly when solar isn't the right move. If your roof needs replacement in three years, we say so. If your shading situation limits production enough to stretch payback beyond 10 years, we show you the numbers. The goal is a system that performs as projected, not a signed contract.

Income-Based Programs Worth Knowing Before You Decide

If upfront cost is the barrier, DC has two programs that change the math significantly. The DCSEU's Solar for All program provides no-cost solar installations for income-qualifying DC residents — no lease, no PPA, no monthly payment. Participants own the benefits of the system without the ownership complexity. The Solar Advantage Plus Program (SAPP), administered through DOEE, offers subsidized installations for moderate-income households. Both programs have waitlists, but both are worth checking before signing any third-party ownership agreement.

For homeowners who don't qualify for income-based programs, a solar loan — where you own the system and pay it off over 10–15 years — typically outperforms a lease on a 20-year horizon in DC, primarily because of SREC income. Our DC solar incentives guide ↗ covers the current program landscape in detail. And if you want to run your own numbers, the SEIA's residential solar resources ↗ provide a useful framework for evaluating financing options.

FAQ

Is it better to lease or purchase solar?

For most DC homeowners in 2026, purchasing is the better financial outcome. Owners keep all SREC income — worth roughly $2,400–$3,600 per year on a typical 7 kW DC system at current market rates of $360–$400/MWh — and benefit from full retail-rate net metering with Pepco. Leasing eliminates upfront cost and provides immediate bill savings, but you forfeit the SREC stream entirely to the third-party owner and carry a 20–25 year contract with annual payment escalators. The federal 25D residential tax credit expired for systems placed in service after December 31, 2025, so that ownership advantage is no longer a factor — but the SREC and net metering economics still favor ownership decisively in DC's market. If upfront cost is the barrier, a solar loan (where you own the system) typically outperforms a lease over a 20-year horizon. Income-qualifying residents should check Solar for All and SAPP before signing any third-party agreement.

What is the 33% rule in solar panels?

There is no single standard “33% rule” in residential solar — the phrase gets used loosely for a few different rules of thumb, which is exactly why it is unreliable. Some advisors use it to mean shading loss should not exceed about a third of potential production; others mean a system should offset at least a third of your annual usage; others apply it to financing, saying a monthly solar payment should not top a third of your electric bill. None of these is an industry standard. Rather than lean on a percentage heuristic, ask for a full production estimate modeled against your actual Pepco bill and a shade analysis of your specific roof — those numbers tell you what any version of the “rule” is only guessing at.

What is the difference between a power purchase agreement and a solar lease?

A solar lease charges a fixed monthly fee regardless of how much electricity the panels produce. A power purchase agreement (PPA) charges per kilowatt-hour actually generated — typically $0.08–$0.14/kWh in 2026. Both arrangements involve third-party ownership of the equipment, meaning you don't own the panels, don't receive SREC income, and carry a lien on your property for the contract term. The practical difference is payment structure: a lease gives you predictable monthly costs, while a PPA payment fluctuates with production. In cloudy months your PPA bill drops; in peak summer months it rises. Both contract types typically run 20–25 years and include annual escalator clauses.

What is the downside of solar lease?

The primary downsides of a solar lease in DC are forfeited SREC income, annual payment escalators, and home sale complications. On SREC income alone, a DC homeowner with a 7 kW system forfeits roughly $3,040 per year at current market rates — income that flows to the leasing company instead. Escalator clauses of 1–3% annually mean your monthly payment grows every year, potentially eroding your savings if utility rates don't keep pace. When you sell your home, the buyer must assume the lease or you must buy out the contract, which can cost $15,000–$25,000 mid-term and has caused home sales to fall through. You also can't claim any tax incentives, and the leasing company files a lien against your property that appears on title searches.

Ready to See Your Numbers Before You Commit?

A Green Zone assessment ↗ gives you a site-specific production estimate, SREC income projection, and honest payback timeline — before any contract is on the table. We'll show you what ownership actually looks like for your roof, your usage, and your goals. No pressure, no expiring offers.